Net Unrealized Appreciation: A Powerful Yet Little Utilized Tax Strategy

- Vince DeCrow

- Jan 8

- 5 min read

If you hold employer stock inside a 401(k) or other qualified retirement plan, taxes can quietly become one of the largest drags on long-term wealth. Most retirement distributions are taxed at ordinary income tax rates, which are often higher than capital gains rates, regardless of how the assets inside the plan performed.

The Net Unrealized Appreciation (NUA) strategy is one of the few exceptions to this rule. When applied correctly, this strategy can significantly reduce lifetime taxes. The unfortunate case is that it is also one of the most misunderstood and underutilized planning strategies available.

What Is Net Unrealized Appreciation?

Net Unrealized Appreciation refers to the difference between the cost basis of employer stock held in a qualified retirement plan and its current market value. In simple terms, it is the built-in gain on company stock that has accumulated while held inside a retirement account, such as a 401(k).

For example, if you acquired company stock inside your 401(k) for $50,000 10 years ago and it is now worth $250,000, the net unrealized appreciation is $200,000. Under traditional retirement plan rules, that entire $250,000 would typically be taxed as ordinary income when distributed to you throughout retirement. The NUA strategy allows for the $200,000 net unrealized appreciation to instead be taxed at long-term capital gains rates.

Given the significant difference between ordinary income and capital gains tax rates for many investors, this distinction can result in substantial tax savings.

How the NUA Strategy Works

The NUA strategy involves a special type of distribution from a qualified retirement plan that holds employer stock. When executed properly, it allows the investor to:

Transfer employer stock “in-kind” from the retirement plan to a taxable brokerage account.

Pay ordinary income tax only on the stock’s original cost basis at the time of the “in-kind” distribution.

Defer taxation on the appreciation until the stock is sold, at which point the gain is generally taxed at long-term capital gains rates.

The remaining assets in the retirement plan (such as bonds, mutual funds, or ETFs), are typically rolled into an IRA, preserving tax deferral but still subject to ordinary income taxes when distributed.

Using the earlier example, if the stock’s cost basis is $50,000, only that amount is taxed as ordinary income when the stock is distributed. The $200,000 of appreciation is not taxed immediately. Instead, it is taxed later when the stock is sold, usually at long-term capital gains rates, regardless of how long the stock is held after distribution.

Key Requirements to Qualify for Favorable NUA Tax Treatment

The rules governing NUA are strict, and any missteps can permanently eliminate the tax benefit. Several conditions must be met:

The distribution must be a lump-sum distribution. A lump-sum distribution means that the entire balance of the qualified plan is distributed within a single tax year. Partial distributions generally do not qualify.

The distribution must follow a triggering event. Triggering events include:

Separation from service

Reaching age 59½

Disability

Death

Employer stock must be distributed in-kind. This means the shares must be transferred directly into a taxable brokerage account. Selling the stock inside the qualified plan before distribution disqualifies it from NUA treatment.

All other plan assets must be fully distributed. Typically, non-employer stock assets in the plan are rolled into an IRA as part of the same transaction. This maintains the tax-deferred treatment of the non-employer stock assets until they’re distributed in retirement years.

Because these rules are unforgiving, professional guidance is not optional. It is essential.

The Tax Benefits of NUA

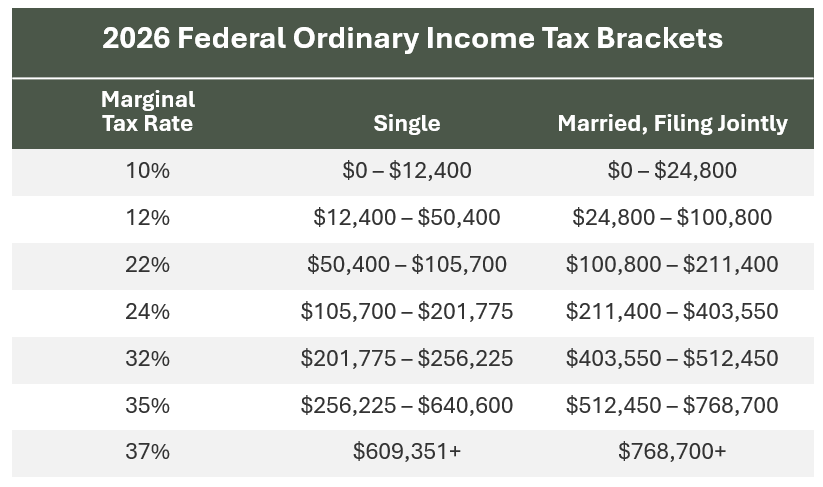

The primary advantage of the NUA strategy is the potential conversion of high ordinary income taxation into more favorable capital gains taxation. For many high earners, Federal ordinary income tax rates can exceed 35%. Long-term capital gains rates, by contrast, are often 15% or 20% at the federal level depending on the investor’s income.

The appreciation is not subject to required minimum distributions (RMDs) once held in a taxable account. If the stock continues to appreciate after distribution, post-distribution gains are taxed under normal capital gains rules.

From a planning perspective, NUA can meaningfully improve after-tax outcomes, especially for investors with highly appreciated employer stock. This treatment is what makes the NUA strategy so compelling.

When NUA May Make Sense

In practice, NUA often makes sense for long-tenured employees of publicly traded companies who accumulated company stock over many years at relatively low prices.

That said, NUA is not an all-or-nothing decision. In some cases, only a portion of the employer stock may be distributed using NUA, while the rest is rolled into an IRA to maintain diversification and risk control.

The NUA strategy is most compelling when certain factors, such as the following, are present:

The employer stock has experienced significant appreciation.

The cost basis of the stock is low relative to its market value.

The investor expects to be in a higher tax bracket in retirement.

The investor is planning to execute a Roth IRA conversion strategy in retirement.

The investor plans to diversify the concentrated stock position over time.

When NUA May Not Be Appropriate

Despite its appeal, NUA is not universally beneficial. Situations where it may not make sense include:

The stock has minimal appreciation.

The investor expects to be in a much lower tax bracket in retirement.

The stock represents an unacceptably large concentration risk.

Liquidity needs or charitable goals favor other planning strategies.

It is also important to recognize that once the NUA election is effectively made, it generally cannot be undone. Poor execution can result in higher taxes than a standard IRA rollover.

Why Professional Planning Matters

The NUA strategy sits at the intersection of tax planning, retirement planning, and investment risk management. While the tax benefits can be substantial, they should never be evaluated in isolation.

Concentration risk, cash flow needs, Medicare premiums, and long-term estate planning objectives all matter. In our view, the best NUA decisions are those that integrate tax efficiency with disciplined diversification and a broader financial plan.

Disclosure

RISE Investment Management, LLC ("RISE" or "RISE Investments") is an investment adviser registered under the Investment Advisers Act of 1940. Registration of an investment adviser does not imply any level of skill or training. This publication is solely for informational purposes and past performance is not indicative of future results. Any description of products, services, and performance results of RISE contained in this publication are not an offering or a solicitation of any kind. No advice may be rendered by RISE Investments unless a client service agreement is in place. Advisory services are only offered to clients or prospective clients where RISE Investments and its representatives are properly licensed or exempt from licensure. All of the information in this publication is believed to be accurate and correct as the date set forth. RISE does not have or accept responsibility or an obligation to update such information. This article is for education purposes and should not be treated as tax or legal advice. This article is not a substitute for legal or tax advice from your professional legal or tax advisor.