Q4 2023 Market Commentary - Federal Reserve Rate Cuts

- Vince DeCrow

- Dec 31, 2023

- 6 min read

U.S. and global markets exceeded expectations in 2023, driven largely by outperformance of the Magnificent Seven mega-cap technology stocks and investor sentiment shifting from “a recession is coming” to “a soft landing and easy monetary policy is around the corner.”

In Q4, the Federal Reserve (Fed) signaled the potential for a series of 2024 rate cuts as inflation cooled throughout the year yet remains above the Fed’s 2.0% target.

Geopolitical risk remains heightened heading into 2024 as violence carries on in Ukraine and the Gaza Strip.

Economic and Market Overview

After one of the most aggressive rate hiking cycles in recent U.S. history, the Fed made a notable shift in policy stance in December as pricing pressures waned. Measured by the Fed’s preferred inflation gauge, the core personal consumption expenditures price index (excludes food and energy), inflation fell to 3.2% in November, its lowest point since March 2021 and well below its peak of 5.6% in February 2023. With inflation trending towards the Fed’s 2% target, the central bank chose to hold rates steady and signaled a change in focus towards when they expect to begin cutting rates in 2024.

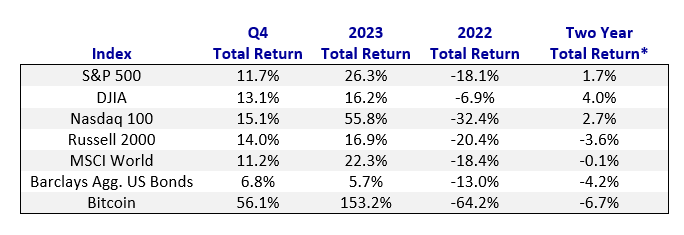

For equity markets, Q4 began with volatility as the rise of long-term interest rates continued and war broke out in the Gaza Strip. However, the combination of strong economic data releases and better-than-expected corporate earnings fueled a swift U-turn of market and investor sentiment in late October. Coupled with new hopes of the Fed cutting interest rates in 2024, global equity markets experienced more powerful rallies over the second half of the quarter than we have seen in recent years, resulting in most U.S. industry sectors ending the year with double-digit total returns.

Equity market performance continued to be dominated by the Magnificent Seven mega-cap technology stocks (AAPL, GOOGL, AMZN, META, TSLA, NVDA, MSFT), propelled by euphorically high investor sentiment as demonstrated by the CNN Fear & Greed Index. When sentiment reaches “greed” levels, certain stock prices tend to be over-extended and present selling opportunities in over-valued stocks. On the flip side, “fear” sentiment typically corresponds with depressed stock prices and long-term buying opportunities for beaten down stocks. The index finished the year with greed levels near their 2023 peak.

Euphoric investor sentiment engulfing the concentrated Magnificent Seven drove the mega-cap technology companies’ valuations to excessive levels through the end of 2023. Outside of the Magnificent Seven, most of the investable universe has underperformed as investor interest waned despite increasingly more attractive valuations amid the surge in inflation and the Fed’s aggressive rate-hiking cycle.

We have tactically maintained an underweight allocation to the Magnificent Seven since early 2022 due to concerns around the euphoric (and record high) valuations of these companies posing excessive risk to your investment portfolios and financial plans. While this underweight allocation to the Magnificent Seven resulted in us missing some of the S&P 500’s gains in 2023, it resulted in offsetting outperformance in 2022. It is important to remember that market diversification and risk-adjusted performance are critical to a successful long-term investment strategy. At RISE, our strategic and tactically managed asset allocations are constructed based on long-term considerations of risk, return, and relationships across asset classes.

The December shift in the Fed’s policy stance also drove a much-needed surge in the fixed income market over the final two months of 2023. The Barclays Aggregate U.S. Bond Index posted a 5.7% total return over the year after suffering a

painful 13% loss in 2022 in the wake of the Fed’s rate hiking cycle. The current bond market presents an inverted yield curve, meaning short-term Treasury bond yields are outpacing longer-maturity yields, which is perceived by some as a signal of a potentially looming economic recession. However, the reliability of the notion that an inverted yield curve means a recession will follow in 100% of cases is questionable. Consumer spending, which represents over 2/3rd of U.S. GDP, remains strong. Corporate balance sheets remain healthy, and capital expenditures continue to hit all-time highs.

2024 Outlook

The global economy continues to be more positive than what consensus predicted at the beginning of 2023, as incredibly stimulative fiscal policy, the resilient labor market, and growing disposable incomes buoyed consumption and spending habits. Barring an exogenous shock, we expect economic growth to continue chugging along in 2024, albeit likely at a slower clip than the 7.5% nominal GDP growth rate recorded in Q3.

Given the pause of Fed rate hikes, reasonable economic growth, and notable investor sentiment, we see a likelihood that the breadth of the market beyond the Magnificent Seven and mega-cap stocks will improve throughout 2024. Our view is that investors will pivot their focus from performance chasing and momentum to fundamental growth and earnings metrics. We currently see several opportunities where positive fundamental stories are not being reflected in market valuations:

Latin American (LatAm) Equities: We see favorable tailwinds for LatAm equities driven by wonderful demographics, China re-shoring initiatives, and cheap relative valuations. As low-end wages have soared in the United States in recent years, remittances from the U.S. to primarily Mexico have gone parabolic, supporting domestic consumption. LatAm equities have strong exposure to critical industries driving the global economy such as basic materials and energy, as well as industries exposed to a growing LatAm middle class such as financials and consumer staples.

Small-Cap Equities: While often regarded as the orphaned cousin of their large-cap brethren, small-cap equities (represented by companies worth between $250 million to $2 billion, net of debt) have outperformed large-caps over the last 25-year period due to their ability to efficiently generate higher relative earnings growth than large-caps. However, small-cap equities have suffered underperformance relative to large-caps over the past decade due to ultra-low borrowing costs that allowed large-caps to magnify their earnings growth with ease. Small-cap equity valuations have become increasingly attractive as a result. Historically, these episodes of medium-term underperformance have created extremely attractive buying opportunities for small-caps based on performance they generated over the subsequent 5-year periods after underperforming large-caps. Today, small-cap equities are valued at 13x future earnings relative to the large-caps at 20x.

Japanese Equities: A generation ago, Japan was the hottest investment in the world going so far that some believed the land under the Emperor’s Imperial Palace was worth more than the entire state of California. Today, the pendulum has completely reversed and Japan’s share in the global equity market cap is a dismal 6% while the U.S.’s weighting is a whopping 63%. While Japan faces headwinds from a shrinking population, we do not believe the current valuation of Japanese equities at 14x future earnings is appropriately pricing-in their current domestic tailwinds. These tailwinds include but aren’t limited to the country’s incredibly productive manufacturing base, historically cheap currency, and reliable supply chain.

Emerging Market (EM) Debt: Largely shrugged off by most Western fixed income investors, EM debt has performed incredibly well despite the most hawkish Federal Reserve policy in decades. Since the Fed stopped quantitative easing in March 2022, the J.P. Morgan EM Local Currency Bond ETF has outperformed the “risk-free” U.S. Treasury Bond by over 25%. In prior tightening cycles, EM debt (and equities) have underperformed as they ran into credit issues with U.S. dollar denominated debt & twin deficit issues. However, the current cycle has proved different. EM debt issuers tend to be nations that are rich in natural resources such as Mexico, Indonesia, Brazil, Malaysia, South Africa, and Columbia. Natural resources such as copper, oil, iron ore, and agriculture are quite valuable in this secular inflation-driven cycle.

Strategic Positioning of Core Portfolios

While 2023 may go down in history as a year of extreme speculation, we believe 2024 is shaping up to look far different than last year and feel strongly that maximizing diversification remains warranted. Periods of euphoria and speculation do not last forever, and the long-term benefits of staying the course with a diversified investment strategy have been proven time and time again over history.

We are privileged to serve as your financial fiduciary and wish you and your family a happy, healthy, and prosperous new year.

Footnotes and Disclosures

*RISE Investment Management, LLC (aka "RISE Investments") is a state Registered Investment Adviser. Registration as an investment advisor does not constitute an endorsement by the Commission and does not imply a certain level of skill or training. Advisory services are only offered to clients or prospective clients where RISE Investments and its representatives are properly licensed or exempt from licensure. This publication is solely for informational purposes and past performance is not indicative of future results. Any historical returns, expected returns, or projections are provided for informational purposes only. No advice may be rendered by RISE Investments unless a client service agreement is in place.