Second Quarter 2025 Market Update and Outlook: The Case for Broader Market Growth

- RISE Investments

- Jul 14, 2025

- 3 min read

Updated: Aug 13, 2025

The equity market swiftly recovered from April’s tariff driven sell-off on the hopes of global trade clarity, interest rate cuts, and fiscal stimulus.

Investor concerns about trade, geopolitics, fiscal, and monetary policy have abated, yet the valuation of the S&P 500 index has returned to generational highs.

Current equity valuations, earnings expectations, and the macro-economic backdrop favor the broader equity market within the U.S.

Market Update

U.S. equities began the quarter with immense volatility driven by President Donald Trump’s proposed tariffs on the country’s largest trading partners. However, investor anxiety eased throughout the quarter with investors focused on tailwinds such as:

Trade Policy Clarity: President Trump announced the removal of reciprocal tariffs on most trade partners

Expectations for Interest Rate Cuts: The Federal Reserve expects two interest rate cuts in the second half of 2025

Fiscal Stimulus: The termination of the Department of Government Efficiency (DOGE) and passage of fiscal stimulus in the U.S. and the European Union

Additional investor worries were driven on the geopolitical front with a brief escalation between Iran and Israel, leading to U.S. participation on behalf of Israel.

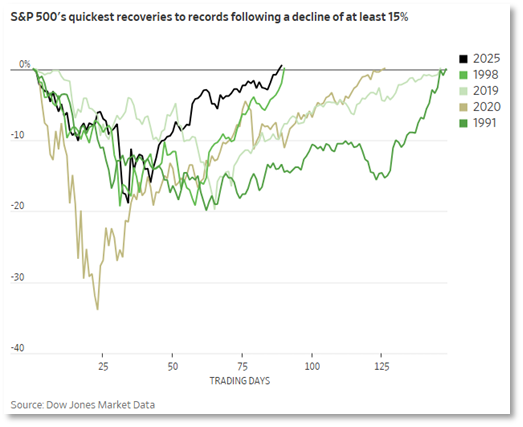

Although plenty of anxieties weighed on investors, equity markets rallied throughout the second quarter with broad equity gains. The recovery from April’s near-term market bottom is one of the fastest reversals in recent memory.

Fixed income market performance varied in the quarter, with corporate fixed income posting positive performance due to tightening credit spreads. Long-term interest rates remained rangebound as investors digested the long-term inflationary impact of fiscal stimulus with that of signaled monetary policy easing.

Economic Update

The U.S. economy showed resilient strength in the second quarter with continued growth in consumption, capital investment, and labor demand. However, the expectation of large Wall Street banks, like Goldman Sachs, going into the quarter was overwhelmingly for a recession.

As we noted in our first quarter letter, our base case remains for U.S. and global economic growth to continue. Recessions are relatively rare and tend to be caused by an exogenous shock to the U.S. and global economy. The natural state of any economy is for growth. Investors that continually wait for a future recession to deploy capital are likely waiting for Godot.

Equity Positioning

We view valuations, earnings expectations, and the positive macro-economic backdrop as favorable for the broader U.S. equity market over the medium-term. This includes areas of the market such as mid cap and small cap domestic equities.

While domestic large cap equities trade at the highest absolute and relative valuations since 2000, valuations of domestic mid cap and small cap equities remain attractive.

Often, and rightfully so, lower valuations are warranted for fundamental reasons. Yet, the differential in earnings growth expectations for domestic large cap equities compared to mid cap and small cap equities is expected to narrow significantly in favor of mid cap and small cap equities.

Furthermore, mid cap and small cap equities offer opportunities for outperformance via stock picking, as these are often overlooked areas of the domestic equity market.

Disclosure

RISE Investment Management, LLC ("RISE" or "RISE Investments") is an investment adviser registered under the Investment Advisers Act of 1940. Registration of an investment adviser does not imply any level of skill or training. This publication is solely for informational purposes and past performance is not indicative of future results. Securities investments are subject to risk and may lose value. Any historical returns, expected returns, or projections are provided for informational purposes only. Any description of products, services, and performance results of RISE contained in this publication are not an offering or a solicitation of any kind. No advice may be rendered by RISE Investments unless a client service agreement is in place. Advisory services are only offered to clients or prospective clients where RISE Investments and its representatives are properly licensed or exempt from licensure. All of the information in this publication is believed to be accurate and correct as the date set forth. RISE does not have or accept responsibility or an obligation to update such information.