When Should I Start Drawing Social Security? How to Determine the Optimal Age

- Vince DeCrow

- May 11

- 5 min read

There’s an age-old question that most individuals begin to think about as they approach retirement; when should I start taking my Social Security retirement benefits?

Claim too early, and you lock in a permanently reduced benefit. Wait too long, and you risk leaving years of income on the table. For most Americans, the difference between the earliest and latest claiming ages can amount to tens of thousands of dollars or more over a lifetime.

So how do you figure out the right time? The answer depends on your health, finances, marital status, and how you think about risk.

Understanding the Basics of Social Security Retirement Benefits

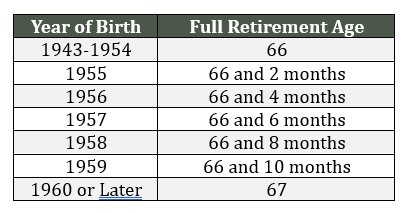

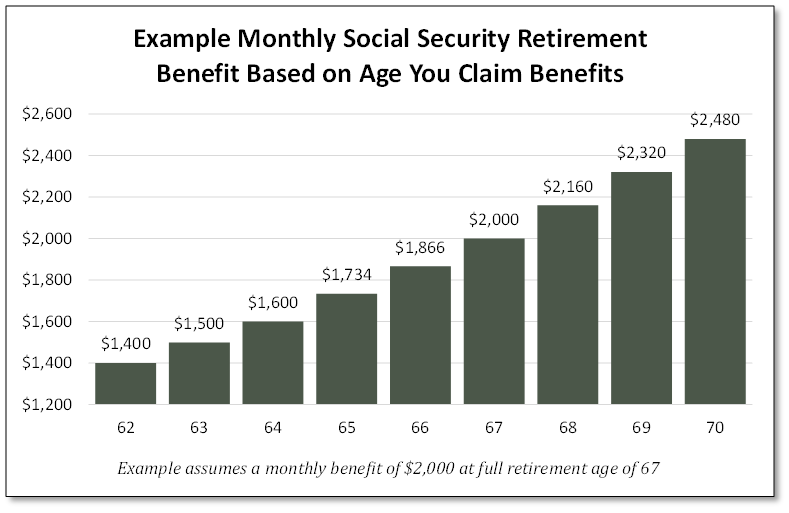

You can begin collecting retirement benefits as early as age 62, but doing so comes at a cost. If you start claiming your benefits at age 62, the monthly benefit amount is permanently reduced by as much as 30% compared to what you'd receive at your Full Retirement Age (FRA). Your FRA is determined by your birth year. For anyone born in 1960 or later, your FRA is 67. You can also delay claiming your benefits until you reach age 70. For every year you wait beyond your FRA (up to 70), your benefit grows by 8%.

For example, if your FRA benefit is $2,000 per month, you would receive as little as $1,400 if claiming at 62, or as much as $2,480 if waiting until 70. That's a difference of roughly $12,960 per year.

The Break-Even Calculation

A common starting point is to conduct a break-even analysis. Break-even represents the age at which the total lifetime benefits from delaying surpasses the total benefits you'd have collected by claiming earlier. Generally, if you claim at 62 instead of 67, you receive five extra years of payments, but each check is smaller. The break-even point typically falls somewhere between ages 78 and 80.

If you expect to live past that age, then delaying tends to pay off financially. If you have serious health concerns or a family history of shorter lifespans, then claiming earlier may make more sense. While this is somewhat of a morbid calculation, Social Security at its core is a form of longevity insurance and the decision should reflect your honest assessment of your own longevity.

Health Is the Single Biggest Variable

No factor matters more than your health. The Social Security Administration's own data shows that average life expectancy for a 65-year-old American today extends well into the mid-to-late 80s. If you're in good health, a non-smoker, and have a family history of longevity, then waiting until age 70 is often the mathematically superior choice. If you're managing a chronic illness or have reason to expect a shorter-than-average lifespan, then claiming earlier can maximize your total lifetime benefit.

Do You Need the Money Now?

For many retirees, the decision often comes down to practicality rather than the mathematically superior choice. If you retire at 62 and have no other income sources to bridge the gap to age 70, then claiming earlier may be your only option.

Burning through your savings or taking on debt while waiting to claim can easily wipe out any gains from the higher monthly benefit, and that is not typically a prudent route to choose.

The ideal scenario for delaying is having sufficient retirement savings, a pension, or a working spouse's income to cover living expenses in the years before you claim. If you can fund your lifestyle without Social Security for several years, then letting your benefit grow by roughly 8% each year you wait is a compelling deal by any investment standard.

Married Couples Have More to Consider

For couples, Social Security timing becomes a coordinated strategy rather than an individual decision. Spousal benefits allow a lower-earning spouse to receive up to 50% of the higher earner's FRA benefit. After the first spouse passes away, the surviving spouse keeps the higher of the two monthly benefits.

This dynamic makes it especially important for the higher-earning spouse to delay as long as possible. By waiting until age 70, the higher earner maximizes not just their own benefit, but also the surviving spouse's benefit that they may eventually need to rely on.

The lower-earning spouse may also consider claiming earlier to bring in income during their higher-earning spouse's delay period.

Working in Retirement

If you plan to keep working after claiming, be aware of the earnings test. If you claim before your FRA and continue working, Social Security will temporarily withhold $1 in benefits for every $2 you earn above $24,480 (2026) and $1 in benefits for every $3 you earn above $65,160 (2026).

Once you reach your FRA, the earnings test disappears and your benefit is recalculated upward to credit the withheld amounts. This doesn't necessarily mean you should avoid claiming while working, but it does add another layer of complexity worth modeling out before you decide.

Taxes Matter Too

Social Security benefits can be partially taxable depending on your total income. If your income (including your Social Security benefit) exceeds $34,000 for individuals or $44,000 for married couples, then up to 85% of your benefit may be taxable.

Delaying Social Security while drawing from a traditional IRA or 401(k) can sometimes reduce your lifetime tax burden by lowering your taxable income in earlier retirement years. This may also shrink your future IRA or 401(k) required minimum distributions.

The Bottom Line

There is no universal right answer to when you should claim Social Security. Rather, the decision is personal and depends on your health, financial resources, marital situation, and retirement goals.

However, if you’re healthy and have adequate retirement savings, then delaying Social Security benefits until age 70 tends to produce the best long-term outcome.

Disclosure

RISE Investment Management, LLC ("RISE" or "RISE Investments") is an investment adviser registered under the Investment Advisers Act of 1940. Registration of an investment adviser does not imply any level of skill or training. This publication is solely for informational purposes and past performance is not indicative of future results. Any description of products, services, and performance results of RISE contained in this publication are not an offering or a solicitation of any kind. No advice may be rendered by RISE Investments unless a client service agreement is in place. Advisory services are only offered to clients or prospective clients where RISE Investments and its representatives are properly licensed or exempt from licensure. All of the information in this publication is believed to be accurate and correct as the date set forth. RISE does not have or accept responsibility or an obligation to update such information. Please note, this article is for education purposes and should not be treated as tax or legal advice. This article is not a substitute for legal or tax advice from your professional legal or tax advisor.